- News

- Subscribe

Get full access to Port Strategy content

Including the print and digital magazines, full news archive, podcasts, webinars and articles on innovations and current trends in the ports and terminals industry.

- Expert analysis and comment

- Unlimited access to in-depth articles and premium content

- Full access to all our online archive

Alternatively REGISTER for website access and sign up for email alerts

- Industry Database

- Events

GreenPort Congress

Green Ports & Shipping Congress

Coastlink Conference

GreenPort Congress is a meeting place for the port community to discuss and learn the latest in sustainable environmental practice. It offers ways to reduce their carbon foot print and be more sensitive to environmental considerations, both of which are vital to future success. The Green Ports & Shipping Congress will identify and prioritise the areas that ports-based organisations and shipping companies need to collaborate on to reduce emissions. Coastlink is a neutral pan-European network dedicated to the promotion of short sea and feeder shipping, and the intermodal transport networks through the ports that support the sector. It is a place for industry professionals to meet and discuss future innovation, economic and environmental considerations – and develop partnerships that will help build a sustainable future. Visit the GPC Website Visit the GPSC Website Visit the Coastlink Website

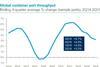

Look beyond trade war, advises Drewry

The US-China trade war may continue to dominate headlines but there are macro-economic factors at work which are “more important” in determining future trade patterns, a ports expert has said.

Continue reading this article…

Register for a FREE one-month trial to continue this article

Want to read more before deciding on a subscription? It only takes a minute to sign up for a free account and you’ll get to enjoy:

- Weekly newsletters providing valuable news and information on the ports and terminals sector

- Full access to our news archive

- Live and archived webinars, podcasts and videos

- Articles on innovations and current trends in the ports and terminals industry

- Our extensive archive of data, research and intelligence

Already subscribed? SIGN IN now

Get more free content sign up today

Ready to subscribe? Choose from one of our subscription packages for unlimited access!